Excel Function For Financial Modeling

I am an Analytical Engineer and I share my learning progress...

Excel is a major modeling tool for Financial Analyst and Financial Modeling.

This post reference can be gotten from Corporate Financial Institute.

Duration Function: is categorized under Financial Functions. it helps to calculate the duration of a security that pays interest on a periodic basis with par value of $100

Duration is commonly used by Portfolio Managers to predict cash flow of investments.

Formula: =DURATION(settlement, maturity, coupon, yield, frequency, [basis])

Settlement: is the security's settlement date or the date on which the coupon is purchased. Maturity: is the security's maturity date or the date on which the coupon expires. Yield: is the the security's annual yield. Frequency: is the number of coupon payments per year. For annual payments, the frequency = 1, for semiannual frequency = 2; and for quarterly frequency = 4. Basis: is the type of day count basis to be used.

The possible values of basis are;

| Basis | Day Count Basis |

| 0 or omitted | US(NASD) 30/360 |

| 1 | Actual/actual |

| 2 | Actual/360 |

| 3 | Actual/365 |

| 4 | European 30/360 |

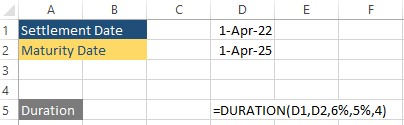

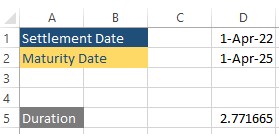

Using Duration Function In Excel Example 1; Let us calculate the duration of a coupon purchased on April 1, 2022 with a maturity date of April 1, 2025 and a coupon rate of 6%. The yield is 5% and payments are made quarterly.

Things to remember about the DURATION Function

#NUM! error - Occurs if either: a. The Supplied Settlement date is >= maturity date; or b. Invalid numbers are supplied for the coupon yield, frequency or [basis] arguments

#VALUE! error - Occurs if either: a. Any of the given arguments is non-numeric or b. One or both of the given settlement or maturity dates are not valid Excel dates.

Settlement, maturity, frequency and basis are truncated to integers